Turning a side hustle into a formal business is more than a mindset shift—it’s a financial strategy. Many entrepreneurs start as sole proprietors, but at a certain income level, forming an LLC can unlock meaningful tax advantages and better long-term scalability. The key is knowing when the switch actually saves you money rather than just adding complexity.

The $30,000 Profit Rule: Calculating Your Self-Employment Tax Savings

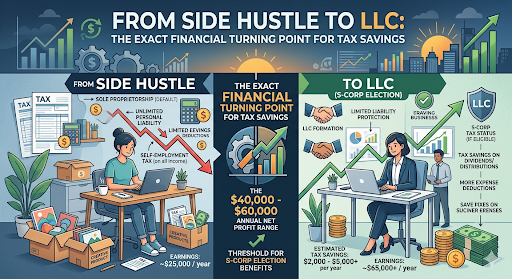

A common financial benchmark for considering an LLC is around $30,000 in annual profit, though the exact number can vary depending on expenses and goals. At this level, self-employment taxes begin to take a noticeable bite out of earnings.

To understand why this matters, you need to break down how much you’re actually paying in taxes as a sole proprietor versus how that burden can shift once you restructure your business.

For many freelancers, consultants, and digital entrepreneurs, this is the point where tax planning becomes more important than just income generation.

Understanding the 15.3% Self-Employment Tax Burden

As a sole proprietor, you are responsible for the full 15.3% self-employment tax, which covers:

- 12.4% for Social Security

- 2.9% for Medicare

Unlike traditional employees, there is no employer splitting the cost—you pay both portions yourself.

This tax applies to your net business income, meaning the more profit you earn, the more you owe. At lower income levels, this is manageable. But as profits grow, this becomes one of the largest tax expenses for small business owners.

This is where strategic restructuring becomes important, especially when your income becomes consistent and predictable.

How the LLC Structure Prepares You for S-Corp Election

Forming an LLC does not automatically change your tax burden—but it does create flexibility.

Once your LLC is established, you can later elect to be taxed as an S-Corporation, which allows you to:

- Pay yourself a “reasonable salary”

- Take remaining profits as distributions (not subject to self-employment tax)

- Reduce overall tax liability when structured correctly

This is why many business owners view the LLC as a stepping stone, not just a legal shield. It creates a foundation for more advanced tax strategies once revenue justifies it.

Comparing Tax Obligations: Sole Prop vs. LLC

The key difference between a sole proprietorship and an LLC is not always the tax rate, it’s how income and deductions are structured and reported.

A sole proprietor and a single-member LLC are taxed similarly by default. However, the LLC provides additional legal separation and optional tax elections that can significantly change your long-term financial outcomes.

Below is a clear comparison of how taxation differs between a sole proprietorship and an LLC structure:

| Feature / Tax Aspect | Sole Proprietor | LLC (Default Taxation) |

| Legal Structure | Not separate entity | Separate legal entity |

| Self-Employment Tax | Paid on all net income | Still applies (default LLC) |

| Tax Filing | Schedule C on personal return | Schedule C or corporate options |

| Liability Protection | None | Yes (personal asset protection) |

| Tax Optimization Options | Limited | High (S-Corp election possible) |

| Credibility with clients | Moderate | Higher |

Passthrough Taxation Explained for Beginners

Both sole proprietorships and LLCs typically operate under pass-through taxation, meaning:

- Business profits are reported on your personal tax return

- The business itself does not pay federal income tax

- You are taxed at individual income tax rates

This system avoids double taxation, but it also means your business income is directly tied to your personal tax liability.

The advantage of an LLC is not immediate tax reduction—it’s the ability to restructure taxation later when your earnings justify it.

Deductible Business Expenses: What Changes After Incorporation?

One of the biggest benefits of moving toward an LLC structure is improved clarity and discipline in expense tracking.

While both sole proprietors and LLC owners can deduct business expenses, LLCs often encourage more structured accounting practices, including:

- Separate business bank accounts

- Cleaner categorization of expenses

- Better audit protection through documentation

Common deductible expenses include:

- Software and subscriptions

- Marketing and advertising

- Home office expenses (if eligible)

- Equipment and tools

- Professional services

The key difference is not what you can deduct, but how efficiently you manage and defend those deductions during tax filing or audits.

Scaling Your Business Revenue Safely

As your side hustle grows, your focus shifts from just earning money to protecting it and optimizing how it is taxed. However, not every stage of growth justifies the complexity of an LLC.

Understanding timing is critical to avoid unnecessary costs and administrative burden.

When Administrative Costs Outweigh Tax Benefits

Forming and maintaining an LLC comes with responsibilities such as:

- State filing fees

- Annual reports

- Accounting or bookkeeping costs

- Possible legal or compliance requirements

For very small businesses or early-stage side hustles, these costs can sometimes exceed the tax benefits.

If your profit is still low or inconsistent, staying a sole proprietor may be more efficient until revenue stabilizes.

The goal is to transition when the financial benefit exceeds operational cost, not simply because it sounds more professional.

Professional Bookkeeping Requirements for New LLCs

Once you form an LLC—especially one preparing for potential S-Corp election—bookkeeping becomes essential, not optional.

Good financial records help you:

- Track deductible expenses accurately

- Separate personal and business finances

- Prepare for tax filings efficiently

- Support future audits or financial reviews

Many growing business owners eventually adopt:

- Accounting software (like QuickBooks or similar tools)

- Monthly financial reconciliation

- Quarterly tax planning sessions

This level of organization ensures that your business is not only growing, but also financially optimized and legally protected.

Conclusion

The transition from side hustle to LLC is not just a legal step—it’s a financial strategy. The real turning point often comes when profits reach a level where self-employment taxes, deductions, and scalability begin to matter significantly.

By understanding the $30,000 profit benchmark, the 15.3% tax burden, and the flexibility of LLC-to-S-Corp planning, entrepreneurs can make informed decisions that maximize long-term savings and business stability.

The right timing isn’t about growth alone it’s about smart growth with tax efficiency in mind.

FAQS

Is an LLC taxed more than a Sole Proprietorship?

No, an LLC is not taxed more than a sole proprietorship by default. Both are usually taxed as pass-through entities, meaning profits are reported on your personal tax return and taxed at the same rates. The difference is in structure and flexibility, not higher taxes.

At what income level does an S-Corp election save money?

An S-Corp election typically becomes beneficial when your net profit consistently exceeds around $50,000–$80,000 per year. At this level, saving on self-employment tax often outweighs the extra payroll and compliance costs.

Does BusinessRocket handle tax registration during formation?

Yes, BusinessRocket typically assists with essential business formation steps, including tax ID (EIN) registration and state compliance setup. However, specific tax filings and ongoing tax strategy are usually handled separately or with a tax professional.

{kind=link}